Foez Dewan

Principal

The Federal Government has progressed a number of legislative initiatives that will impact on directors and are likely to come into effect in 2019 if they go ahead. The proposed new laws include significantly increasing civil and criminal penalties for breaches of the Corporations Act 2001 (Cth), introducing a new Director Identification Number regime and making directors personally liable for the unpaid GST debts of their companies.

Proposed new legislation will see some changes for directors that are likely to happen in 2019 if the legislation is introduced and passed. These include:

So, what do these proposed changes mean for directors?

The introduction of the Penalties Bill is a clear response to the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry (Royal Commission), with a significant change to penalties.

The Commonwealth Treasury warns that the Penalties Bill “… would double maximum imprisonment penalties for some of the most serious ‘white-collar’ criminal offences bringing Australia’s penalties in closer alignment with leading international jurisdictions”.2

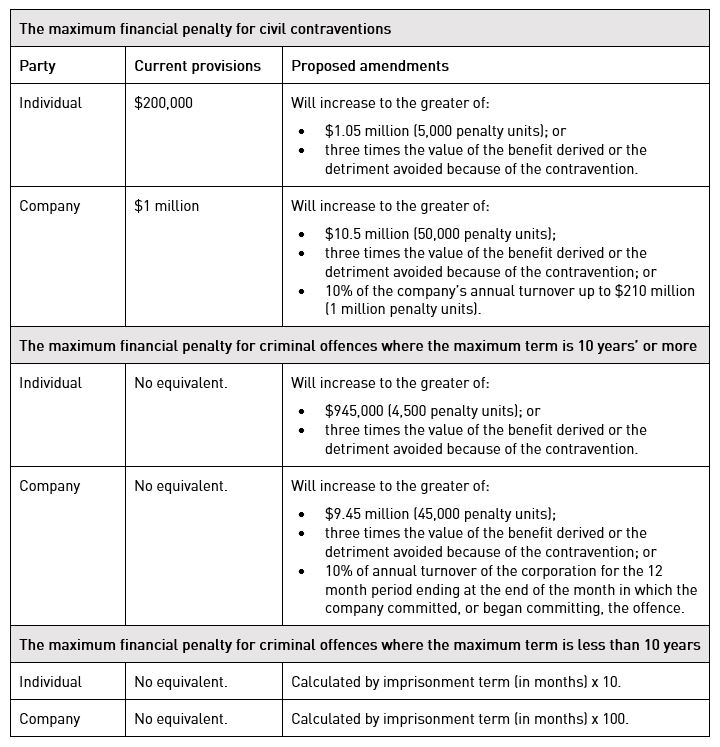

The Penalties Bill proposes to significantly increase the civil and criminal penalties for breaches of the Corporations Act 2001 (Cth) from the current penalties, as summarised below, and also introduces new formulae to calculate the maximum penalties for civil and criminal contraventions as summarised below:

(1) A director or other officer of a corporation commits an offence if they:

(1) A director or other officer of a corporation commits an offence if they:

(a) are reckless; or

(b) are intentionally dishonest;

and fail to exercise their powers and discharge their duties:

(c) in good faith in the best interests of the corporation; or

(d) for a proper purpose.

The amendment will erase the requirement to prove the director (and other officers) intentionally acted dishonestly and failed to discharge his/her duties in acting in the best interests of the corporation.

The impact of the proposed changes and the introduction of an objective test for dishonesty is that directors who consider their conduct as honest or may not have intended or known that their conduct was dishonest may still be found to have contravened the Corporations Act such as liability under subsections 184(2) and 184(3) for dishonest use of position or information, and section 588G for dishonestly trading while insolvent.

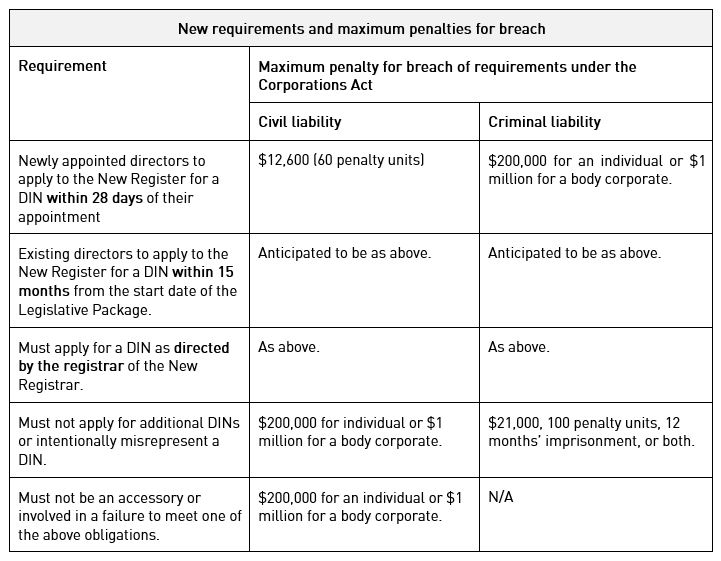

Under the draft Legislative Package,3 it is proposed to introduce a requirement that each registered director applies for and obtains a unique Director Identification Number (DIN) under a newly inserted Part 9.1A of the Corporations Act and Part 6-7A of the Corporations (Aboriginal and Torres Strait Islander) Act 2006 (Cth).

In addition to the DIN requirement, the draft Legislative Package proposes to consolidate Australia’s thirty-five business registries administered by ASIC and the Australian Business Registry (ABR) (New Register). Operating alongside the DIN requirement, both changes should improve the traceability of directors’ relationships between entities and to better track illegal phoenix activities.

The following table summarises the proposed new obligations directors will have in respect of DINs and the maximum penalties for breaches of those obligations:

2 Treasurer of the Commonwealth of Australia, ‘Government consults on stronger penalties for corporate and financial sector misconduct’ (Joint Media Release, 26 September 2018) 3.

2 Treasurer of the Commonwealth of Australia, ‘Government consults on stronger penalties for corporate and financial sector misconduct’ (Joint Media Release, 26 September 2018) 3.

3 The Treasury Laws Amendment (Registries Modernisation and Other Measures) Bill 2018 proposes to amend the Corporations Act and the Corporations (Aboriginal and Torres Strait Islander) Act 2006.

4 Set out in Division 269 in Schedule 1 of the Taxation Administration Act 1953 (Cth) (Taxation Administration Act).

In June 2023, a Canadian Court in South-West Terminal Ltd v Achter Land and Cattle Ltd, 2023 SKKB 116, held that the "thumbs-up" emoji carried enough weight to constitute acceptance of contractual terms, analogous to that of a "signature", to establish a legally binding contract. Facts This case involved a contractual dispute between two parties namely South-West Terminal ("SWT"), a grain and crop inputs company; and Achter Land & Cattle Ltd ("ALC"), a farming corporation. SWT sought to purchase several tonnes of flax at a price of $17 per bushel, and in March 2021, Mr Mickleborough, SWT's Farm Marketing Representative, sent a "blast" text message to several sellers indicating this intention. Following this text message, Mr Mickleborough spoke with Mr Achter, owner of ALC, whereby both parties verbally agreed by phone that ALC would supply 86 metric tonnes of flax to SWT at a price of $17 per bushel, in November 2021. After the phone call, Mr Mickleborough applied his ink signature to the contract, took a photo of it on his mobile phone and texted it to Mr Archter with the text message, "please confirm flax contract". Mr Archter responded by texting back a "thumbs-up" emoji, but ultimately did not deliver the 87 metric tonnes of flax as agreed. Issues The parties did not dispute the facts, but rather, "disagreed as to whether there was a formal meeting of the minds" and intention to enter into a legally binding agreement. The primary issue that the Court was tasked with deciding was whether Mr Achter's use of the thumbs-up emoji carried the same weight as a signature to signify acceptance of the terms of the alleged contract. Mr Mickleborough put forward the argument that the emoji sent by Mr Achter conveyed acceptance of the terms of the agreement, however Mr Achter disagreed arguing that his use of the emoji was his way of confirming receipt of the text message. By way of affidavit, Mr Achter stated "I deny that he accepted the thumbs-up emoji as a digital signature of the incomplete contract"; and "I did not have time to review the Flax agreement and merely wanted to indicate that I did receive his text message." Consensus Ad Idem In deciding this issue, the Court needed to determine whether there had been a "formal meeting of the minds". At paragraph [18], Justice Keene considered the reasonable bystander test: " The court is to look at “how each party’s conduct would appear to a reasonable person in the position of the other party” (Aga at para 35). The test for agreement to a contract for legal purposes is whether the parties have indicated to the outside world, in the form of the objective reasonable bystander, their intention to contract and the terms of such contract (Aga at para 36). The question is not what the parties subjectively had in mind, but rather whether their conduct was such that a reasonable person would conclude that they had intended to be bound (Aga at para 37)." Justice Keene considered several factors including: The nature of the business relationship, notably that Mr Achter had a long-standing business relationship with SWT going back to at least 2015 when Mr Mickleborough started with SWT; and The consistency in the manner by which the parties conducted their business by way of verbal conversation either in person or over the phone to come to an agreement on price and volume of grain, which would be followed by Mr Mickleborough drafting a contract and sending it to Mr Achter. Mr Mickleborough stated, "I have done approximately fifteen to twenty contracts with Achter"; and The fact that the parties had both clearly understood responses by Mr Achter such as "looks good", "ok" or "yup" to mean confirmation of the contract and "not a mere acknowledgment of the receipt of the contract" by Mr Achter. Judgment At paragraph [36], Keene J said: "I am satisfied on the balance of probabilities that Chris okayed or approved the contract just like he had done before except this time he used a thumbs-up emoji. In my opinion, when considering all of the circumstances that meant approval of the flax contract and not simply that he had received the contract and was going to think about it. In my view a reasonable bystander knowing all of the background would come to the objective understanding that the parties had reached consensus ad item – a meeting of the minds – just like they had done on numerous other occasions." The court satisfied that the use of the thumbs-up emoji paralleled the prior abbreviated texts that the parties had used to confirm agreement ("looks good", "yup" and "ok"). This approach had become the established way the parties conducted their business relationship. Significance of the Thumbs-Up Emoji Justice Keene acknowledged the significance of a thumbs-up emoji as something analogous to a signature at paragraph [63]: "This court readily acknowledges that a thumbs-up emoji is a non-traditional means to "sign" a document but nevertheless under these circumstances this was a valid way to convey the two purposes of a "signature" – to identify the signator… and… to convey Achter's acceptance of the flax contract." In support of this, Justice Keene cited the dictionary.com definition of the thumbs-up emoji: "used to express assent, approval or encouragement in digital communications, especially in western cultures", confirming that the thumbs-up emoji is an "action in an electronic form" that can be used to allow express acceptance as contemplated under the Canadian Electronic Information and Documents Act 2000. Justice Keene dismissed the concerns raised by the defence that accepting the thumbs up emoji as a sign of agreement would "open the flood gates" to new interpretations of other emojis, such as the 'fist bump' and 'handshake'. Significantly, the Court held, "I agree this case is novel (at least in Skatchewan), but nevertheless this Court cannot (nor should it) attempt to stem the tide of technology and common usage." Ultimately the Court found in favour of SWT, holding that there was a valid contract between the parties and that the defendant breached by failing to deliver the flax. Keene J made a judgment against ALC for damages in the amount of $82,200.21 payable to SWT plus interest. What does this mean for Australia? This is a Canadian decision meaning that it is not precedent in Australia. However, an Australian court is well within its rights to consider this judgment when dealing with matters that come before it with similar circumstances. This judgment is a reminder that the common law of contract has and will continue to evolve to meet the everchanging realities and challenges of our day-to-day lives. As time has progressed, we have seen the courts transition from sole acceptance of the traditional "wet ink" signature, to electronic signatures. Electronic signatures are legally recognised in Australia and are provided for by the Electronic Transactions Act 1999 and the Electronic Transactions Regulations 2020. Companies are also now able to execute certain documents via electronic means under s 127 of the Corporations Act. We have also seen the rise of electronic platforms such as "DocuSign" used in commercial relationships to facilitate the efficient signing of contracts. Furthermore, this case highlights how courts will interpret the element of "intention" when determining whether a valid contract has been formed, confirming the long-standing principle that it is to be assessed objectively from the perspective of a reasonable and objective bystander who is aware of all the relevant facts. Overall, this is an interesting development for parties engaging in commerce via electronic means and an important reminder to all to be conscious of the fact that contracts have the potential to be agreed to by use of an emoji in today's digital age.

The McCabes Government team are pleased to have assisted Venues NSW in successfully overturning a District Court decision holding it liable in negligence for injuries sustained by a patron who slipped and fell down a set of steps at a sports stadium; Venues NSW v Kane [2023] NSWCA 192 Principles The NSW Court of Appeal has reaffirmed the principles regarding the interpretation of the matters to be considered under sections5B of the Civil Liability Act 2002 (NSW). There is no obligation in negligence for an occupier to ensure that handrails are applied to all sets of steps in its premises. An occupier will not automatically be liable in negligence if its premises are not compliant with the Building Code of Australia (BCA). Background The plaintiff commenced proceedings in the District Court of NSW against Venues NSW (VNSW) alleging she suffered injuries when she fell down a set of steps at McDonald Jones Stadium in Newcastle on 6 July 2019. The plaintiff attended the Stadium with her husband and friend to watch an NRL rugby league match. It was raining heavily on the day. The plaintiff alleged she slipped and fell while descending a stepped aisle which comprised of concrete steps between rows of seating. The plaintiff sued VNSW in negligence alleging the stepped aisle constituted a "stairwell" under the BCA and therefore ought to have had a handrail. The plaintiff also alleged that the chamfered edge of the steps exceeded the allowed tolerance of 5mm. The Decision at Trial In finding in favour of the plaintiff, Norton DCJ found that: the steps constituted a "stairwell" and therefore were in breach of the BCA due to the absence of a handrail and the presence of a chamfered edge exceeding 5mm in length. even if handrails were not required, the use of them would have been good and reasonable practice given the stadium was open during periods of darkness, inclement weather, and used by a persons of varying levels of physical agility. VNSW ought to have arranged a risk assessment of the entire stadium, particularly the areas which provided access along stepped surfaces. installation of a handrail (or building stairs with the required chamfered edge) would not impose a serious burden on VNSW, even if required on other similar steps. Issues on Appeal VNSW appealed the decision of Norton DCJ. The primary challenge was to the trial judge's finding that VNSW was in breach of its duty of care in failing to install a handrail. In addition, VNSW challenged the findings that the steps met the definition of a 'stairwell' under the BCA as well as the trial judge's assessment of damages. Decision on Appeal The Court of Appeal found that primary judge's finding of breach of duty on the part of VNSW could not stand for multiple reasons, including that it proceeded on an erroneous construction of s5B of the Civil Liability Act 2002 and the obvious nature of the danger presented by the steps. As to the determination of breach of duty, the Court stressed that the trial judge was wrong to proceed on the basis that the Court simply has regard to each of the seven matters raised in ss 5B and 5C of the CLA and then express a conclusion as to breach. Instead, the Court emphasised that s 5B(1)(c) is a gateway, such that a plaintiff who fails to satisfy that provision cannot succeed, with the matters raised in s 5B(2) being mandatory considerations to be borne in mind when determining s 5B(1)(c). Ultimately, regarding the primary question of breach of duty, the Court found that: The stadium contained hazards which were utterly familiar and obvious to any spectator, namely, steps which needed to be navigated to get to and to leave from the tiered seating. While the trial judge considered the mandatory requirements required by s5B(2) of the CLA, those matters are not exhaustive and the trial judge failed to pay proper to attention to the fact that: the stadium had been certified as BCA compliant eight years before the incident; there was no evidence of previous falls resulting in injury despite the stairs being used by millions of spectators over the previous eight years; and the horizontal surfaces of the steps were highly slip resistant when wet. In light of the above, the Court of Appeal did not accept a reasonable person in the position of VNSW would not have installed a handrail along the stepped aisle. The burden of taking the complained of precautions includes to address similar risks of harm throughout the stadium, i.e. installing handrails on the other stepped aisles. This was a mandatory consideration under s5C(a) which was not properly taken into account. As to the question of BCA compliance, the Court of Appeal did not consider it necessary to make a firm conclusion of this issue given it did not find a breach of duty. The Court did however indicated it did not consider the stepped aisle would constitute a "stairway" under the BCA. The Court of Appeal also found that there was nothing in the trial judge's reasons explicitly connecting the risk assessment she considered VNSW ought to have carried out, with the installation of handrails on any of the aisles in the stadium and therefore could not lead to any findings regarding breach or causation. As to quantum, the Court of Appeal accepted that the trial judge erred in awarding the plaintiff a "buffer" of $10,000 for past economic loss in circumstances where there was no evidence of any loss of income. The Court of Appeal set aside the orders of the District Court and entered judgment for VNSW with costs. Why this case is important? The case confirms there is no obligation in negligence for owners and operators of public or private venues in NSW to have a handrail on every set of steps. It is also a welcome affirmation of the principles surrounding the assessment of breach of duty under s 5B and s 5C of the CLA, particularly in assessing whether precautions are required to be taken in response to hazards which are familiar and obvious to a reasonable person.

The recent decision in New Aim Pty Ltd v Leung [2023] FCAFC 67 (New Aim) has provided some useful guidance in relation to briefing experts in litigation.